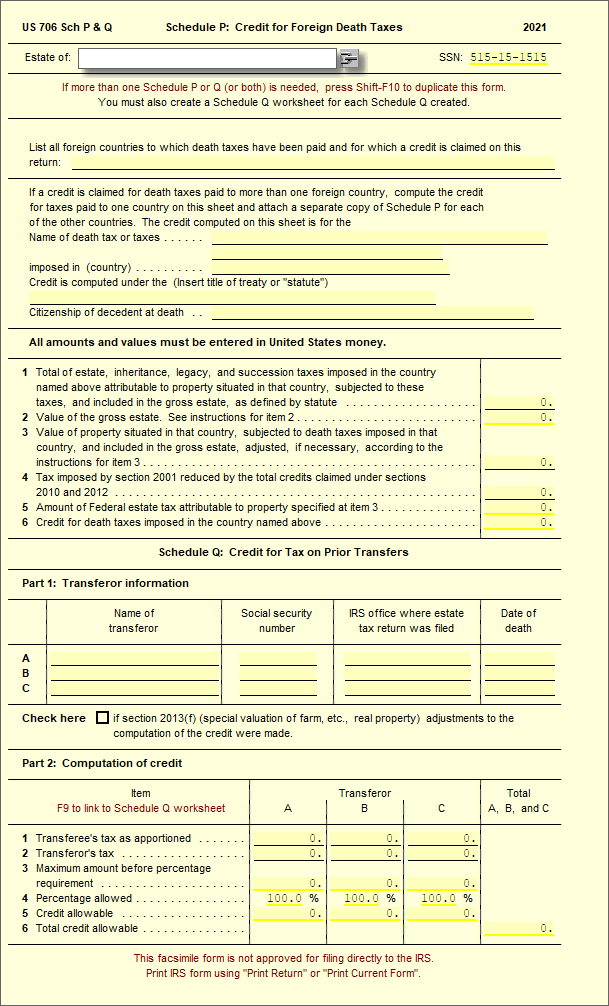

What is the form used for? : SCH P

- The credit for foreign death taxes is allowable only if the decedent was a citizen or resident of the United States.

- However, see section 2053(d) and the related regulations for exceptions and limitations if the executor has elected, in certain cases, to deduct these taxes from the value of the gross estate.

- For a resident, not a citizen, who was a citizen or subject of a foreign country for which the President has proclaimed under section 2014(h), the credit is allowable only if the country of which the decedent was a national allows a similar credit to decedents who were U.S. citizens residing in that country.

What is the form used for? : SCH Q

- The term “transferee” means the decedent for whose estate this return is filed. If the transferee received property from a transferor who died 10 years before or 2 years after the transferee, a credit is allowable on this return for all or part of the federal estate tax paid by the transferor's estate for the transfer.

- There is no requirement that the property is identified in the estate of the transferee or that it exists on the date of the transferee's death. It is sufficient for the credit allowance that the property transfer was subjected to federal estate tax in the estate of the transferor and that the specified period has not elapsed.

- A credit may be allowed for property received as the result of the exercise or non-exercise of a power of appointment when the property is included in the gross estate of the power.

Is the form Supported in our program? Yes

How to access the form: To access the form, you will need to open a 706 return on the desktop and then go to Add Form/Display, and type 706 P and Q.

Limits to the form: This form can only be accessed from the desktop software. This form cannot be copied.

IRS Publication: https://www.irs.gov/pub/irs-pdf/i706.pdf

Comments

Article is closed for comments.